What is a profit & loss statement?

A plain-English look at one of the most useful reports in your business — what it is, what it's for, and how it's put together.

The short version

A profit and loss statement — usually shortened to "P&L," and sometimes called an income statement — is a one-page summary of what your business earned and what it spent over a period of time. Subtract the spending from the earning, and you've got your profit (or loss) for that period. That's really it.

What it's for

A P&L answers a question every business owner needs to be able to answer: am I actually making money? Your bank balance alone can be misleading — a fat account might just mean a big tax bill is coming, and a thin one doesn't necessarily mean the business is unhealthy. A P&L cuts through that by lining up income and expenses side by side.

In practice, people use P&Ls to:

- File accurate tax returns (your tax preparer will ask for one)

- Spot which services or products are actually profitable

- Catch expenses that have quietly crept up over time

- Apply for a loan, a lease, or a line of credit

- Decide whether you can afford to hire, raise rates, or take time off

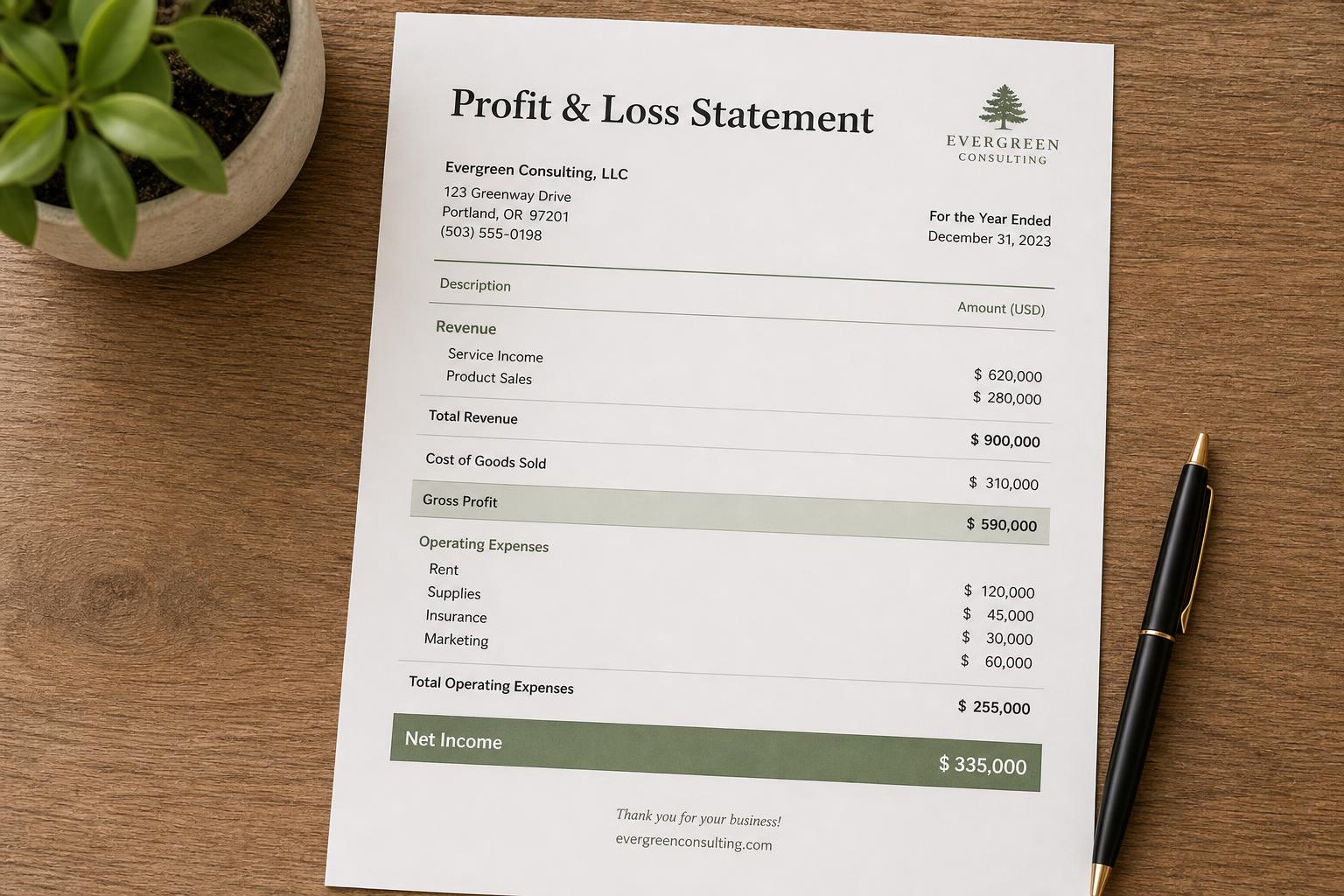

How it's structured

Almost every P&L follows the same basic shape. You start at the top with money coming in, subtract costs as you go, and end at the bottom with what's left over — which is why people call net income the "bottom line."

- Revenue (Income)

All the money your business brought in from sales or services during the period.

- Cost of Goods Sold (COGS)

The direct costs of delivering what you sold — materials, wholesale product costs, or anything that only exists because you made a sale.

- Gross Profit

Revenue minus COGS. This is what you have left to cover the rest of running the business.

- Operating Expenses

The ongoing costs of being open — rent, software, insurance, marketing, professional fees, and so on.

- Net Income (the bottom line)

Gross profit minus operating expenses. A positive number is a profit; a negative number is a loss.

Bigger businesses add more layers — interest, depreciation, taxes — but the core idea is the same: revenue at the top, expenses subtracted in groups, profit at the bottom.

How often should you look at one?

At minimum, once a year for taxes. But a monthly or quarterly P&L is where the real value shows up — it turns "I think things are going okay" into actual numbers you can act on. Most bookkeeping software can generate one in a couple of clicks once your transactions are categorized.

Ready to build your own?

If you'd like a step-by-step walk-through with example categories for a wellness practice, head over to our companion article on how to create a profit & loss statement. And if you'd rather hand it off entirely, that's something we can help with too — get in touch.